Industrial Revolution

Wastewater from industrial production and its potential for treatment and reuse presents an opportunity for market growth in a range of industries. In its latest Insight Report, “Industrial Wastewater Treatment and Water Re-Use in Six Key Industries,” BlueTech Research evaluated the market potential for these key industries: pulp and paper, brewing, dairy, chemical, pharmaceutical, and meat and poultry. The report further detailed market drivers and barriers, major wastewater treatment and reuse technology providers, and future technology opportunities available in the wastewater treatment and water reuse market.

Water is utilized in a variety of capacities within industrial processes—washing, mixing, cooling, etc.—presenting the potential for water treatment and reuse; however, water does not play an equal role in each industry, with certain industries incorporating higher volumes of water into their production processes, leading to differing market potentials among the six key industries.

Wastewater Volumes

The report found that the pulp and paper industry generated the highest volume of wastewater compared with the other industries analyzed, with 898 million gal per day (mgd) (3.4 million cu meters per day) in the U.S. and 977 mgd (3.7 million cu meters per day) in the European Union. In terms of the total value of economic output, however, the pulp and paper industry represented the smallest value when compared with the other industries: $302 million. The food and beverage industry—which takes into account the dairy, brewing, and meat and poultry industries—generates approximately 547 mgd (2.07 million cu meters per day) of wastewater in the U.S. and 573 mgd (2.17 million cu meters per day) in the European Union, but presents a market opportunity of $1.9 billion for wastewater treatment systems. For further comparison, Figure 1 captures the volume of wastewater produced in both the U.S. and European Union in all six key industries.

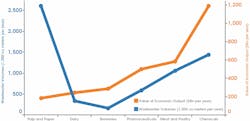

Volumes & Economic Output Value

Ultimately, higher volumes of wastewater produced do not equal higher market opportunities. Figure 2 explains the relationship between wastewater volumes produced and the value of economic output by industry sector, which shows the market potential for the remaining industries analyzed in this report.

Several market barriers account for the differences in the wastewater volumes produced and potential economic opportunity for water reuse and treatment in each industry, particularly in the pulp and paper industry. Pulp and paper mills generate significant volumes of wastewater, but despite high water usage, reuse of pulp and paper mill effluent is relatively rare, as mills are generally located in remote areas with large supplies of freshwater. The industry has a reputation of being highly adverse to risk and in most cases does not invest in new technologies to improve operations unless the return on investment (ROI) is extremely competitive—less than four years ROI in some cases.

In North America, several mills have incorporated effluent reuse technologies, such as the zero liquid discharge treatment facility at the Meadow Lake pulp mill in Saskatchewan, Canada; however, these were designed for site-specific circumstances and are not indicative of an overall market trend for mills in the North American market. On the other hand, European mills show more interest in water reuse due to high water rates and discharge surcharges, as they are a significant cost burden to the mills.

More Market Barriers

Another market barrier is the cost of treating wastewater to a potable quality. In the food and beverage industry, many companies will not consider reusing treated effluent for product water due to negative public perception, as it is deemed “dirty” water. Various state and federal authorities require water that makes contact with the final food product to meet the U.S. Environmental Protection Agency’s potable quality standards. These processes (e.g., vat cleaning in brewing, eviscerating in a slaughterhouse) comprise the majority of water usage in facilities; up to 90% in certain industries. To reach an acceptable potable water quality, several tertiary treatment processes, including reverse osmosis, would be required, making reuse water more expensive relative to conventional water sources. Overall, the cost of wastewater treatment does not entice many companies in the food and beverage industry to adopt water reuse technologies, as the costs do not outweigh the convenience of conventional water sources.

Market Growth Drivers

While these market barriers hinder market opportunities, there also are elements driving market growth. Corporate social responsibility (CSR) pushes industries to meet cumulative goals and targets related to environmental performance and enhanced sustainability set out in their environmental management systems. CSR drives industries to reduce their impact on the environment, and subsequently decrease their emissions, carbon footprint and water use. As companies strive for positive public perception and a commitment to the environment, this proves promising for water reuse on site.

The food and beverage industry in particular is trying to address sustainability. Even though water reuse poses a cost versus convenience issue, several companies in the brewing and soft drink sector—such as Miller, Coors and Coca-Cola—are changing the wastewater treatment landscape in the industry and have begun to develop sustainability plans that include reducing the product water usage ratio (water used per unit of product). Reuse and recycling of effluent have been identified as key components to reach these conservation targets. While the technology required to produce potable reuse water from effluent is more advanced than conventional treatment systems, several companies in the food and beverage industry are driving forward regardless of the cost to maintain a positive public image.

Identifying Opportunities

Looking to the future, BlueTech Research identifies industrial wastewater treatment technology opportunities. These include resource recovery, particularly non-product water reuse—such as water from washing, boiler feed and cooling

towers—and water reuse with innovative technology offerings, such as anaerobic membrane bioreactors, which increase water reuse on site and diminish the quantity of sludge produced, while reducing overall cost and energy consumption.

More comprehensive analysis on the industrial wastewater and water reuse market, including specific technology opportunities and active innovative companies in the industry, is available in BlueTech Research’s Insight Report, “Industrial Wastewater Treatment and Water Re-Use in Six Key Industries.”

Download: Here